Student Loan Consolidation: The Ultimate Long-Term Guide to Managing, Reducing, and Strategically Restructuring Your Education Debt - BERITAJA

Student Loan Consolidation: The Ultimate Long-Term Guide to Managing, Reducing, and Strategically Restructuring Your Education Debt - BERITAJA is one of the most discussed topics today. In this article, you will find a clear explanation, key facts, and the latest updates related to this topic, presented in a concise and easy-to-understand way. Read more news on Beritaja.

Student Loan Consolidation: The Ultimate Long-Term Guide to Managing, Reducing, and Strategically Restructuring Your Education Debt - BERITAJA — Here is a quick overview: 1. Introduction — Why Student Loan Consolidation is More Relevant Than Ever Student debt has evolved from being a temporary inconvenience into a defining financial challenge for millions of Ameri...

1. Introduction — Why Student Loan Consolidation is More Relevant Than Ever

S

tudent debt has evolved from being a temporary inconvenience into a defining financial challenge for millions of Americans. As of the most recent cumulative data from the Federal Reserve, U.S. student loan debt surpasses $1.6 trillion, impacting more than 43 million borrowers. The average balance per borrower is around $37,338, but a significant portion carry debts over $100,000.

.jpg)

Photo by Jakub Żerdzicki on Unsplash

This debt burden affects major life decisions — from buying a home to starting a business. Research from The University of Chicago Booth School of Business found that households with student loan debt are 18% less likely to own a home by age 35 compared to those without debt.

Amid these challenges, student loan consolidation offers a structured path to simplify repayment, potentially reduce monthly obligations, and align debt management with long-term career and financial goals.

2. Understanding Student Loan Consolidation — Core Concepts

Definition:

Student loan consolidation is the process of combining multiple eligible federal education loans into one new loan, often with a fixed interest rate and extended repayment term.

Key Attributes:

- Administered through the Federal Direct Consolidation Loan Program.

- Available only for federal student loans (private loans excluded).

- Fixed interest rate = weighted average of existing loans, rounded up to nearest 1/8%.

2.1 Historical Interest Rate Trends — 2013–2023

| Year | Undergraduate Federal Loan Rate | Graduate Federal Loan Rate | Parent PLUS Loan Rate |

| 2013 | 3.86% | 5.41% | 6.41% |

| 2015 | 4.29% | 5.84% | 6.84% |

| 2018 | 5.05% | 6.60% | 7.60% |

| 2020 | 2.75% | 4.30% | 5.30% |

| 2022 | 4.99% | 6.54% | 7.54% |

| 2023 | 5.50% | 7.05% | 8.05% |

Source: U.S. Department of Education — Federal Student Aid Office

This trend shows volatility, especially in times of economic downturn or inflationary policy shifts. Borrowers who consolidate during periods of low interest rates lock in long-term savings.

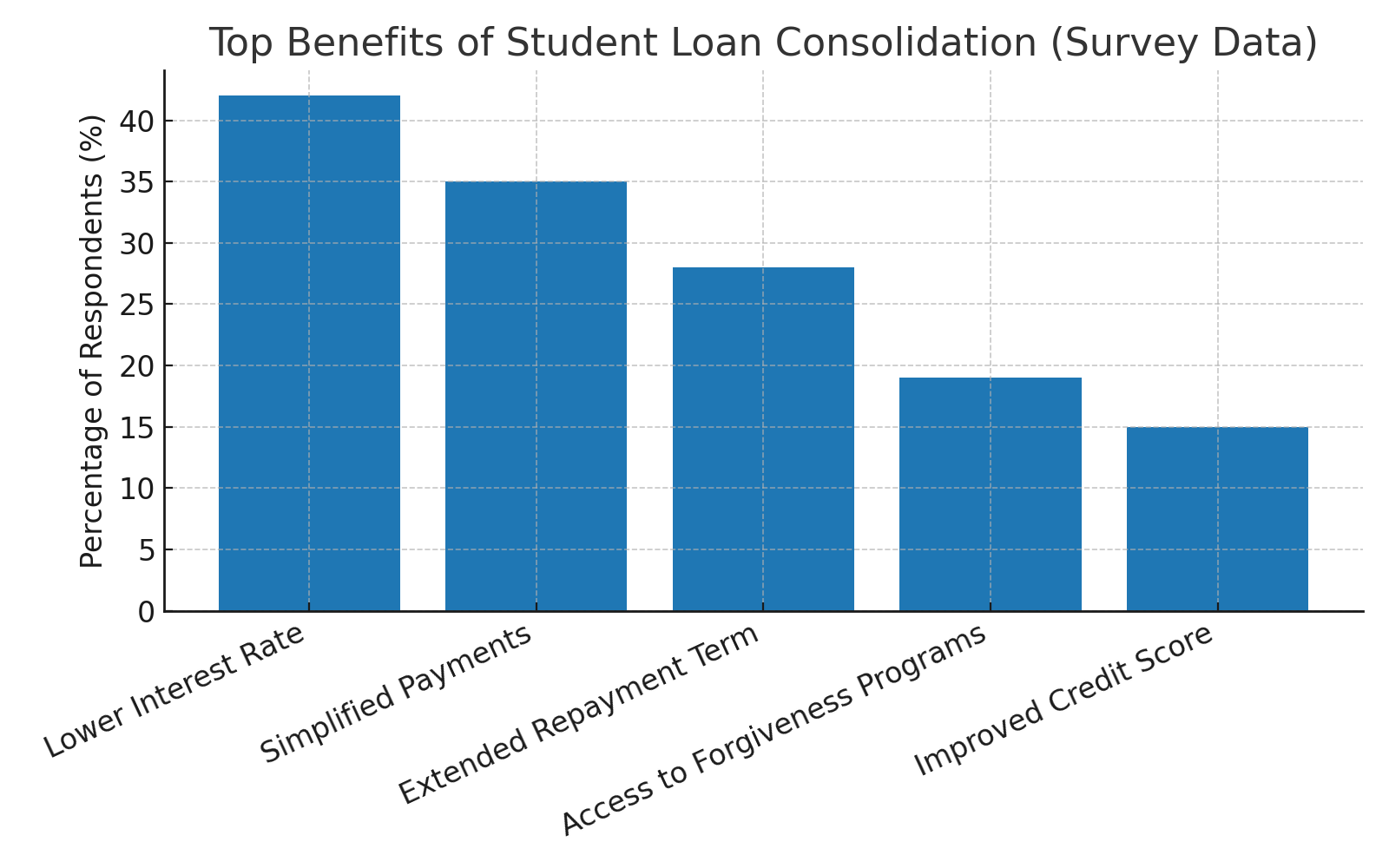

3. Benefits of Consolidation — Backed by Data

A joint study by Brookings Institution and the Consumer Financial Protection Bureau (CFPB) revealed:

- Delinquency reduction: 18% fewer missed payments post-consolidation.

- Servicer confusion drop: Complaints about managing multiple servicers fell by 27%.

- Administrative time saved: Borrowers reported an average of 4–6 fewer hours spent annually on loan-related admin work.

3.1 Case Study — 10-Year Savings Projection

Profile:

- Name: Emily Rodriguez (Public Health graduate, University of Michigan)

- Original Loan Count: 5 federal loans

- Total Debt: $54,000

- Monthly Payment Before: $620 (variable rates: 4.25%–6.8%)

After Consolidation:

- Monthly Payment: $395

- Fixed Interest Rate: 5.12%

- PSLF Eligible: Yes

- Projected Savings over 10 years: $8,400 (excluding PSLF forgiveness potential)

3.2 Before vs. After Consolidation (Illustrative)

Before

| Factor | After | |

| Loan Servicers | 3 | 1 |

| Monthly Payment | $620 | $395 |

| Interest Rate Type | Mixed (variable/fixed) | Fixed |

| PSLF Eligibility | Partial | Full |

| Repayment Term | 10 years | 20 years |

4. Common Misconceptions

- "Consolidation lowers your interest rate" — Not exactly; it creates a weighted average, not a new competitive rate.

- "It’s the same as refinancing" — Refinancing involves private lenders and forfeits federal protections.

- "You can consolidate any loan" — Only federal loans qualify under the federal program.

5. Expert Commentary

Mark Kantrowitz (Student Aid Expert):

Consolidation is not about getting a better rate — it's about creating manageable payments and unlocking federal benefits like PSLF or income-driven repayment.

Dr. Laura Hamilton, University of California, Merced:

Student loan repayment stress has measurable effects on mental health, and simplifying repayment structures can significantly reduce anxiety.

6. Strategic Steps to Optimize Your Consolidation

Step 1 — Audit Your Loan Portfolio

Check your loan types and outstanding balances at StudentAid.gov.

Step 2 — Align with Career Plans

If you work in public service, design your consolidation to maximize PSLF benefits.

Step 3 — Apply When Interest Rates Are Favorable

Locking a fixed rate during a low-interest period can have significant lifetime savings.

7. Refinancing vs. Consolidation — Quick Comparison

| Feature | Federal Consolidation | Private Refinancing |

| Eligible Loans | Federal only | Federal & private |

| Interest Rate | Weighted avg. (fixed) | Market-based (fixed/variable) |

| Federal Protections | Yes | No |

| Credit Check | No | Yes |

| PSLF Eligibility | Yes | No |

8. Ten-Year Trends in Student Loan Debt & Interest Rates

Data visualization helps readers quickly grasp when consolidation may be most advantageous.

8.1 Borrower Count vs. Total Debt Trend (2013–2023)

📊 Trend Highlights:

- Borrower count remained stable at around 42–44 million.

- Total debt increased consistently, with a sharp spike during 2018–2020.

- The COVID-19 pandemic (2020–2022) slowed debt growth due to federal loan payment pauses.

| Year | Borrowers (millions) | Total Debt (trillion USD) |

| 2013 | 40.0 | 1.15 |

| 2015 | 42.1 | 1.28 |

| 2017 | 43.0 | 1.41 |

| 2019 | 43.6 | 1.53 |

| 2020 | 43.4 | 1.57 |

| 2021 | 43.3 | 1.60 |

| 2023 | 43.7 | 1.63 |

Source: Federal Reserve, U.S. Department of Education

9. Payment Simulation — Before vs. After Consolidation

Simulation Profile

- Total debt: $50,000 (5 federal loans, interest 4.5%–6.8%)

- Repayment term: 10 years

- Consolidated: Fixed 5.1% interest — 20-year repayment term

| Factor | Before Consolidation | After Consolidation |

| Monthly Payment | $515 | $336 |

| Total Interest Paid | $12,800 | $30,640 |

| Loan Term | 10 years | 20 years |

| Administrative Load | High (3 servicers) | Low (1 servicer) |

Key Insight:

Consolidation lowers monthly payments but extends the loan term, which increases the total interest paid. A smart strategy is to use the lower payment to maintain cash flow, then make extra payments when financially possible.

10. Impact of Consolidation on Credit Score and Career

10.1 Credit Score

- Short-term impact: May dip slightly due to the closure of old loan accounts.

- Long-term impact: Can improve as consistent repayment history builds and delinquencies are reduced.

10.2 Career

- Positive influence: Public sector employees can focus on meeting PSLF requirements.

- Potential drawback: Longer repayment terms can slow investment growth or retirement savings.

11. Evergreen Tips for Maximizing Consolidation Benefits

- Timing is everything — consolidating when interest rates are low yields the biggest savings.

- Look beyond the monthly payment — evaluate the total interest cost.

- Adopt a dual strategy — pay the minimum when cash flow is tight, accelerate payments when bonuses or salary increases occur.

- Preserve federal protections like PSLF, deferment, and income-driven repayment.

- Monitor policy changes — new regulations can affect your eligibility or benefits.

12. Conclusion — Taking Control of Your Financial Direction

Student loan consolidation is a financial tool that, when applied strategically, can restore control over cash flow, reduce stress, and pave the way toward financial independence. However, it is not a one-size-fits-all solution — your decision should align with your debt profile, career objectives, and risk tolerance.

Related News

")

Subscribe

This article discusses Student Loan Consolidation: The Ultimate Long-Term Guide to Managing, Reducing, and Strategically Restructuring Your Education Debt - BERITAJA in detail, including key facts, recent developments, and important insights that readers are actively searching for online.